Payment System

7 min readDesign a payment backend for an e-commerce application (e.g. Amazon.com). Handles all money movement.

Step 1 - Understand the Problem and Establish Design Scope

Requirements:

- Payment backend for e-commerce (Amazon-like)

- Supports credit cards, PayPal, bank cards (focus on credit cards for interview)

- Uses third-party payment processors (Stripe, Braintree, Square) — NOT direct processing

- Does NOT store credit card data internally (security/compliance)

- Global, but single currency assumed

- 1 million transactions/day

- Supports pay-in flow (money from buyers to platform) and pay-out flow (money to sellers)

- Reconciliation required (fix inconsistencies between internal + external services)

Non-functional: reliability/fault tolerance, reconciliation process (async verification across systems).

Back-of-the-envelope: 1M transactions / 86,400 sec ≈ 10 TPS. Low throughput → focus is on correctness, not raw scale.

Step 2 - Propose High-Level Design and Get Buy-In

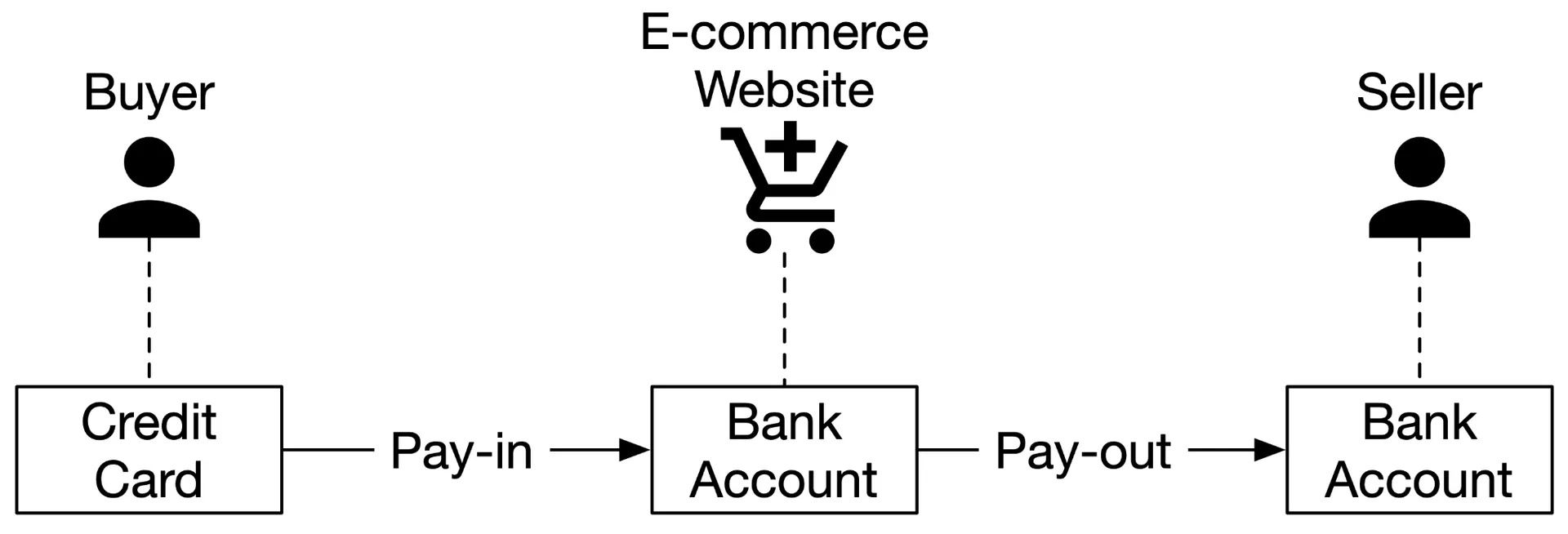

Pay-in flow

Figure 1: Simplified pay-in and pay-out flow

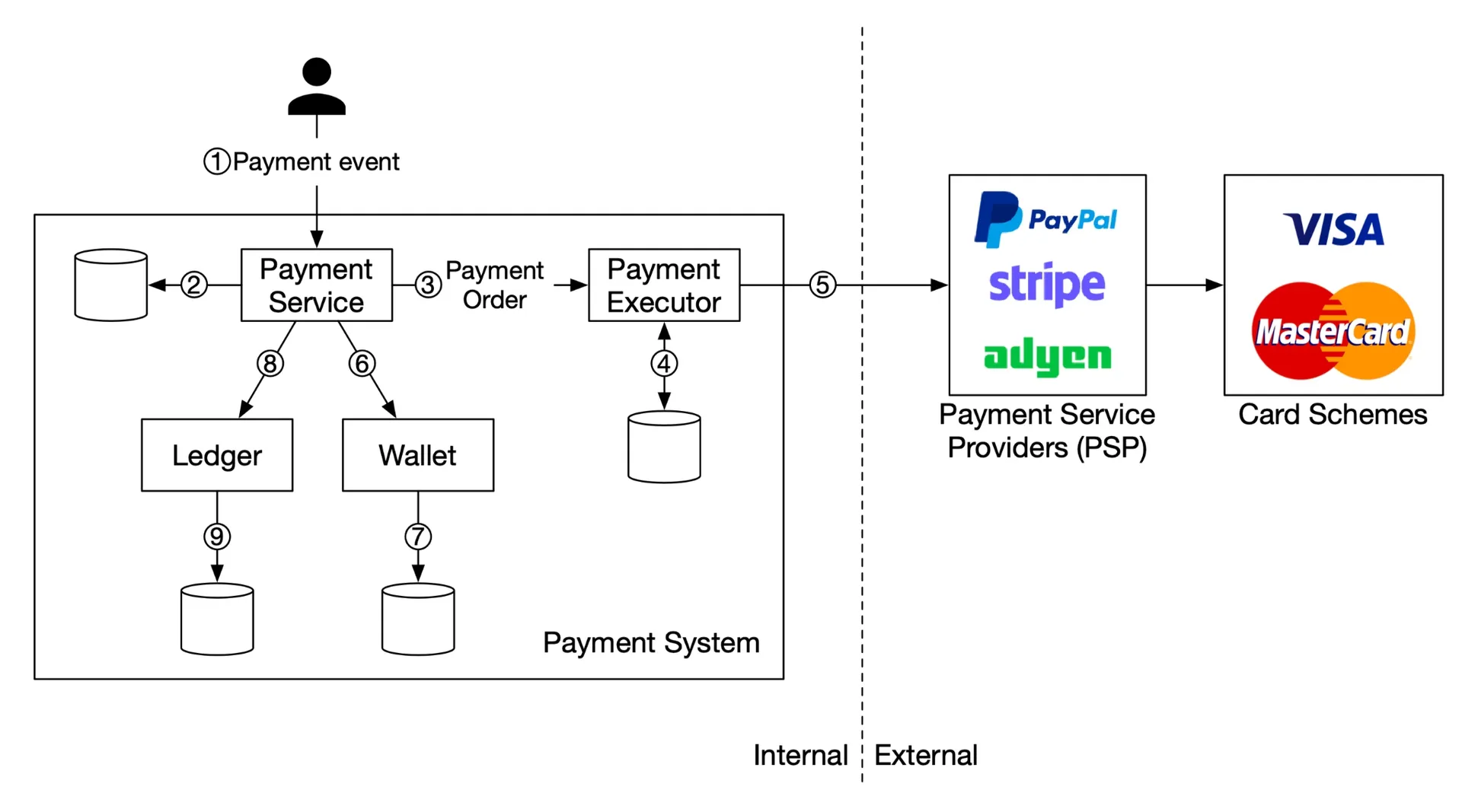

Figure 2: Pay-in flow

Components:

- Payment service: accepts payment events, coordinates process. First runs risk check (AML/CFT compliance, fraud detection — typically third-party).

- Payment executor: executes single payment order via PSP. One payment event may contain multiple payment orders.

- PSP (Payment Service Provider): moves money from buyer's credit card to platform's bank account.

- Card schemes: Visa, MasterCard, Discover — process credit card operations.

- Ledger: financial record (debit buyer 1,creditseller1, credit seller 1). Used for post-payment analysis (revenue, forecasting).

- Wallet: merchant account balance. Records total amount paid per user.

Pay-in flow steps:

- User clicks "place order" → payment event → payment service

- Payment service stores event in DB

- Single checkout may split into multiple payment orders (products from multiple sellers). Payment service calls payment executor for each.

- Payment executor stores payment order in DB

- Payment executor calls external PSP to process credit card

- On success: payment service updates wallet (seller balance)

- Wallet server stores updated balance

- Payment service calls ledger

- Ledger appends new entry

Payment service APIs

POST /v1/payments — Execute payment event. Params: buyer_info, checkout_id (globally unique), credit_card_info (encrypted or token), payment_orders list.

Each payment_order: seller_account, amount (string, not double), currency (ISO 4217), payment_order_id (globally unique, used as PSP dedup/idempotency key).

Why string for amount: different protocols/hardware have different numeric precision → rounding errors. Numbers can be extremely large (Japan GDP ~5×10¹⁴ yen) or small (satoshi = 10⁻⁸ BTC). Parse to number only for display/calculation.

GET /v1/payments/{:id} — Get payment order execution status by payment_order_id.

Data model

Storage choice factors: proven stability (5+ years in big financial firms), monitoring/investigation tools, DBA job market maturity. → Traditional relational DB with ACID over NoSQL/NewSQL.

Payment event table:

| Name | Type |

|---|---|

| checkout_id | string PK |

| buyer_info | string |

| seller_info | string |

| credit_card_info | depends on provider |

| is_payment_done | boolean |

Payment order table:

| Name | Type |

|---|---|

| payment_order_id | String PK |

| buyer_account | string |

| amount | string |

| currency | string |

| checkout_id | string FK |

| payment_order_status | string (enum) |

| ledger_updated | boolean |

| wallet_updated | boolean |

Status states: NOT_STARTED → EXECUTING → SUCCESS / FAILED. On SUCCESS: update wallet (wallet_updated = TRUE) → update ledger (ledger_updated = TRUE). All orders under same checkout_id succeed → is_payment_done = TRUE. Scheduled job monitors in-flight orders, alerts on threshold exceeding.

Key insight: Pay-in moves money from buyer's credit card → platform's bank account (not seller's). Seller gets money via pay-out flow when conditions met (e.g. product delivered).

Double-entry ledger system

Every transaction recorded in two ledger accounts with same amount. Sum of all entries = 0. One cent lost = someone gains a cent. End-to-end traceability. See Square's immutable double-entry accounting DB.

| Account | Debit | Credit |

|---|---|---|

| buyer | $1 | |

| seller | $1 |

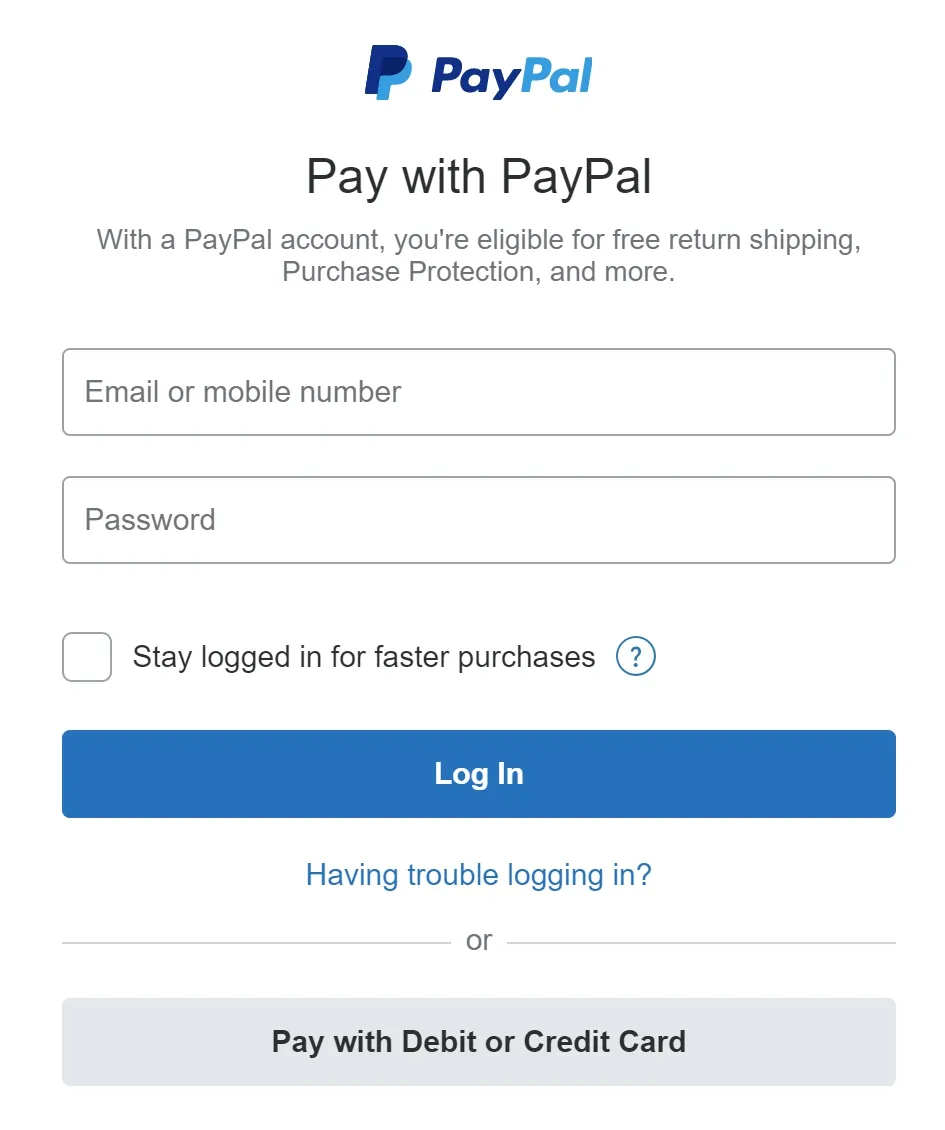

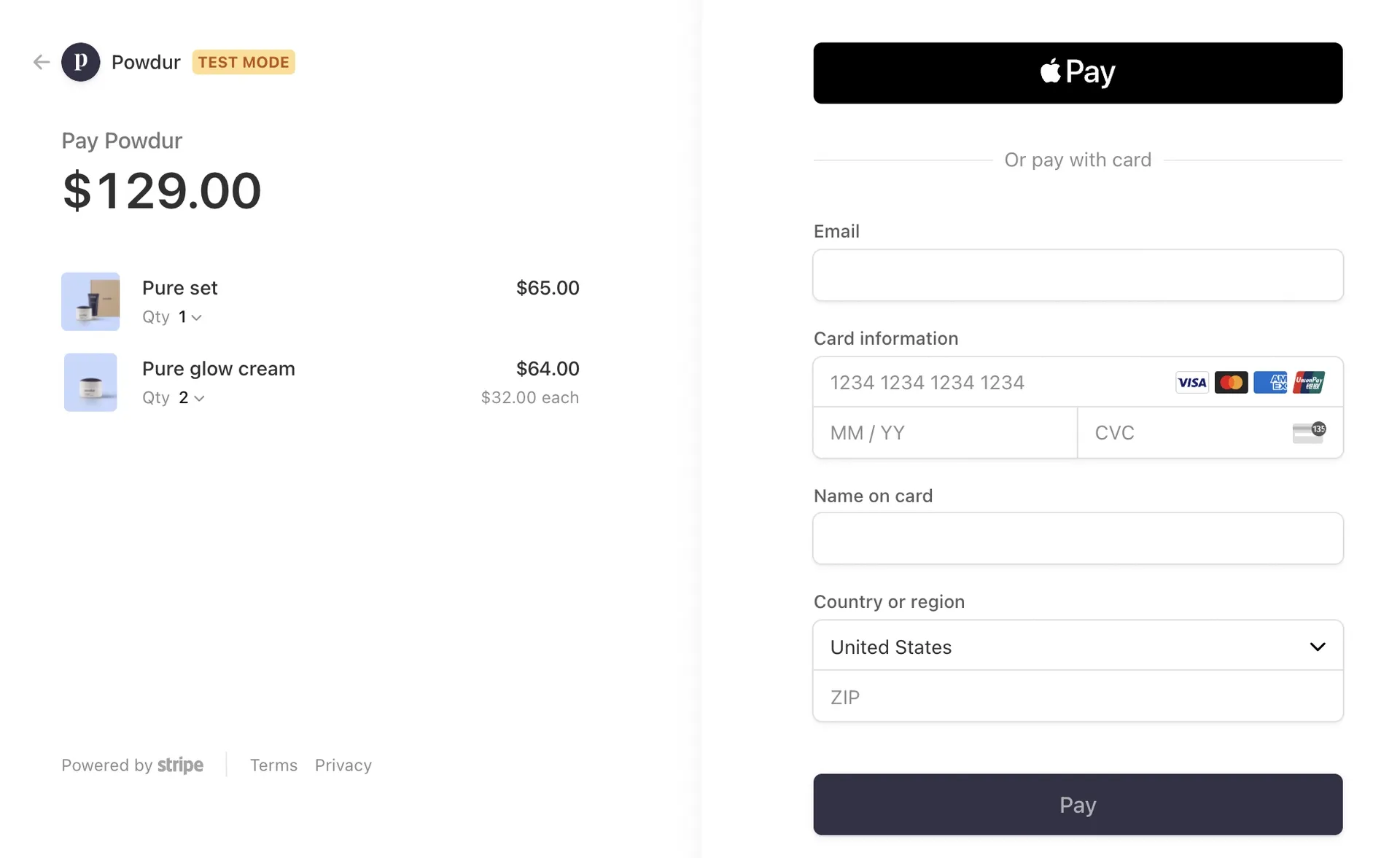

Hosted payment page

Companies avoid storing credit cards (PCI DSS compliance burden). PSP provides hosted page (widget/iframe for web, SDK for mobile). PSP collects sensitive data directly — never reaches our payment system.

Figure 3: Hosted pay with PayPal page

Pay-out flow

Similar to pay-in but uses third-party pay-out provider (e.g. Tipalti) to move money from platform bank account → seller bank account. Additional bookkeeping/regulatory requirements.

Step 3 - Design Deep Dive

PSP integration

Two approaches:

- Direct API: company stores payment info, develops payment pages. PSP connects to banks/card schemes.

- Hosted payment page (common): PSP provides page, collects/stores card data. Company avoids PCI DSS.

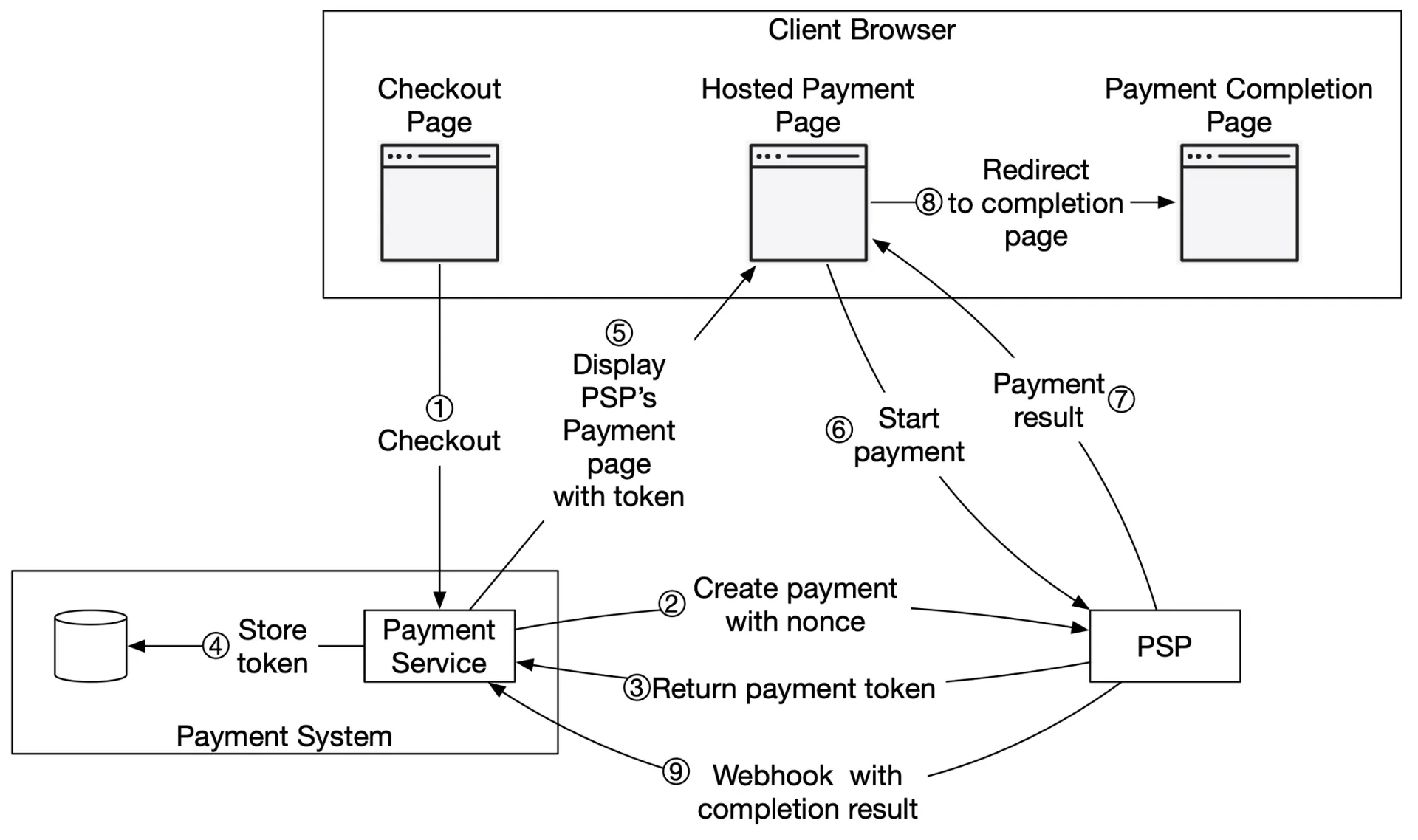

Hosted payment flow:

Figure 4: Hosted payment flow

- Client clicks "checkout" → payment service with payment order info

- Payment service → PSP: payment registration request (amount, currency, expiration, redirect URL, nonce = payment_order_id for exactly-once registration)

- PSP returns token (UUID, uniquely identifies registration)

- Payment service stores token in DB

- Client displays PSP-hosted payment page (Stripe JS library). Needs: token + redirect URL.

Figure 5: Hosted payment page by Stripe

- User fills card details on PSP page → clicks pay → PSP processes

- PSP returns payment status

- Browser redirected to redirect URL (status appended as query param)

- Async: PSP calls payment service via webhook with payment status. Payment service updates

payment_order_status.

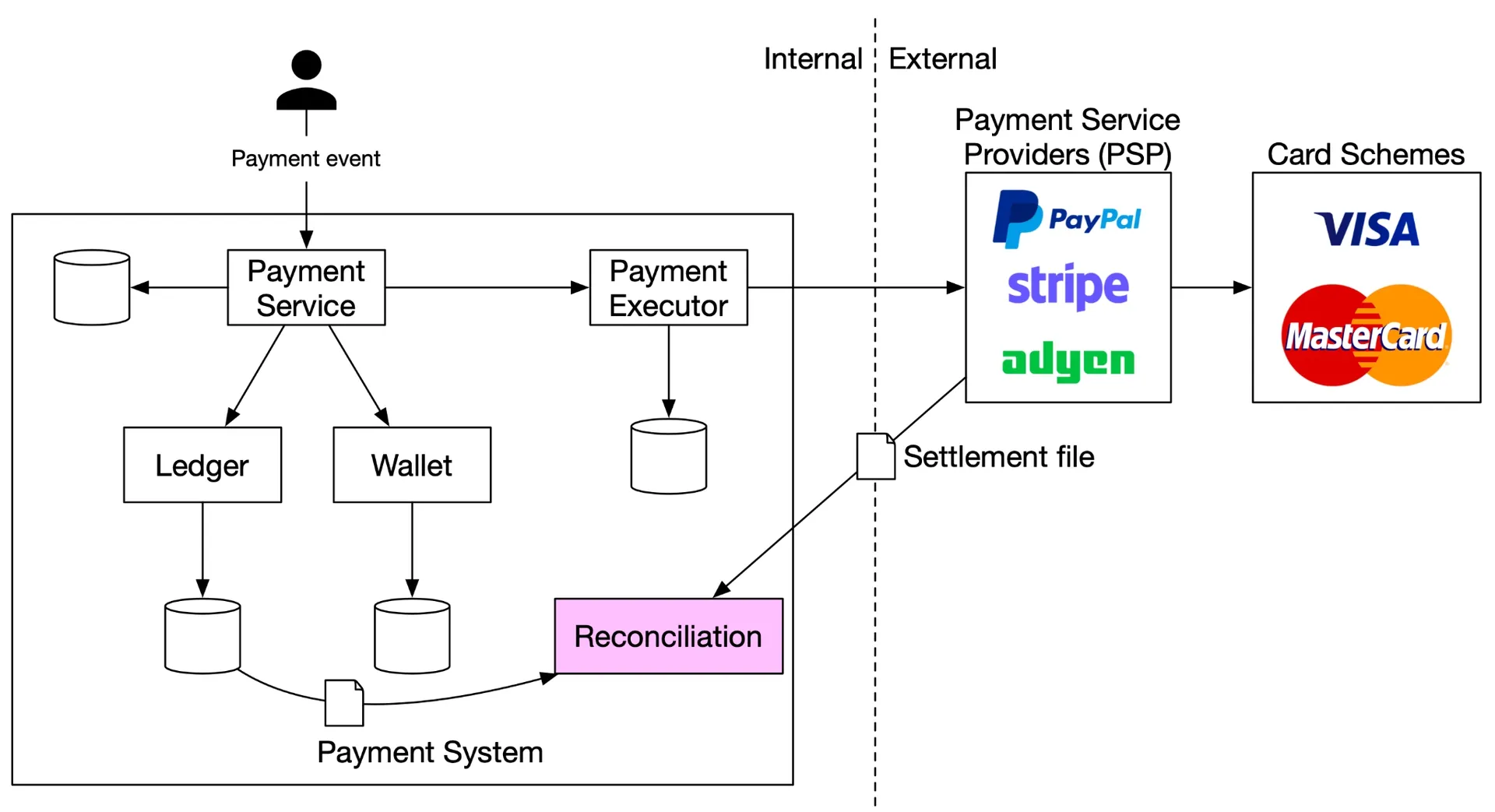

Reconciliation

Async communication → no guaranteed delivery. Reconciliation periodically compares states across related services — last line of defense.

Figure 6: Reconciliation

Nightly: PSP/banks send settlement file (bank balance + daily transactions). Reconciliation system parses and compares with ledger.

Also used internally (ledger vs. wallet divergence detection).

Mismatch handling:

- Classifiable + automatable: auto-fix via code

- Classifiable, not automatable: manual fix by finance team (job queue)

- Unclassifiable: special queue, finance team investigates

Handling payment processing delays

Some payments take hours/days (PSP risk review, 3D Secure Authentication). PSP handles long-running requests:

- Returns pending status to client. Client shows pending + check-status page.

- PSP notifies via webhook on status change (or payment service polls PSP).

Three-party consistency (client, payment service, PSP) requires idempotency + reconciliation.

Communication among internal services

Synchronous (HTTP):

- Cons: low performance (one slow service impacts all), poor failure isolation, tight coupling, hard to scale

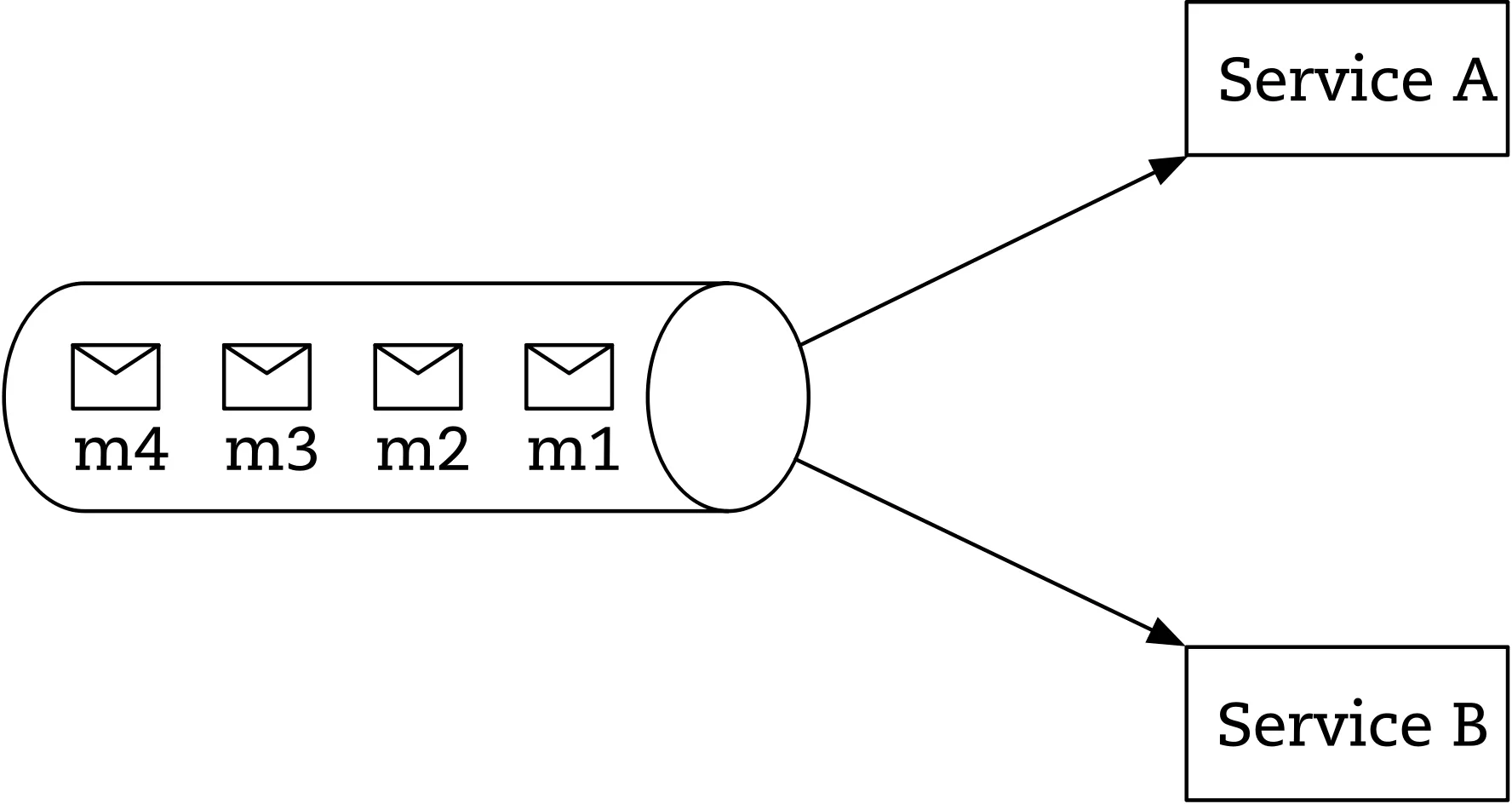

Asynchronous (message queue/Kafka):

-

Single receiver: shared message queue. Once processed, message removed.

Figures 7-8: Message queue, single receiver

Figures 7-8: Message queue, single receiver -

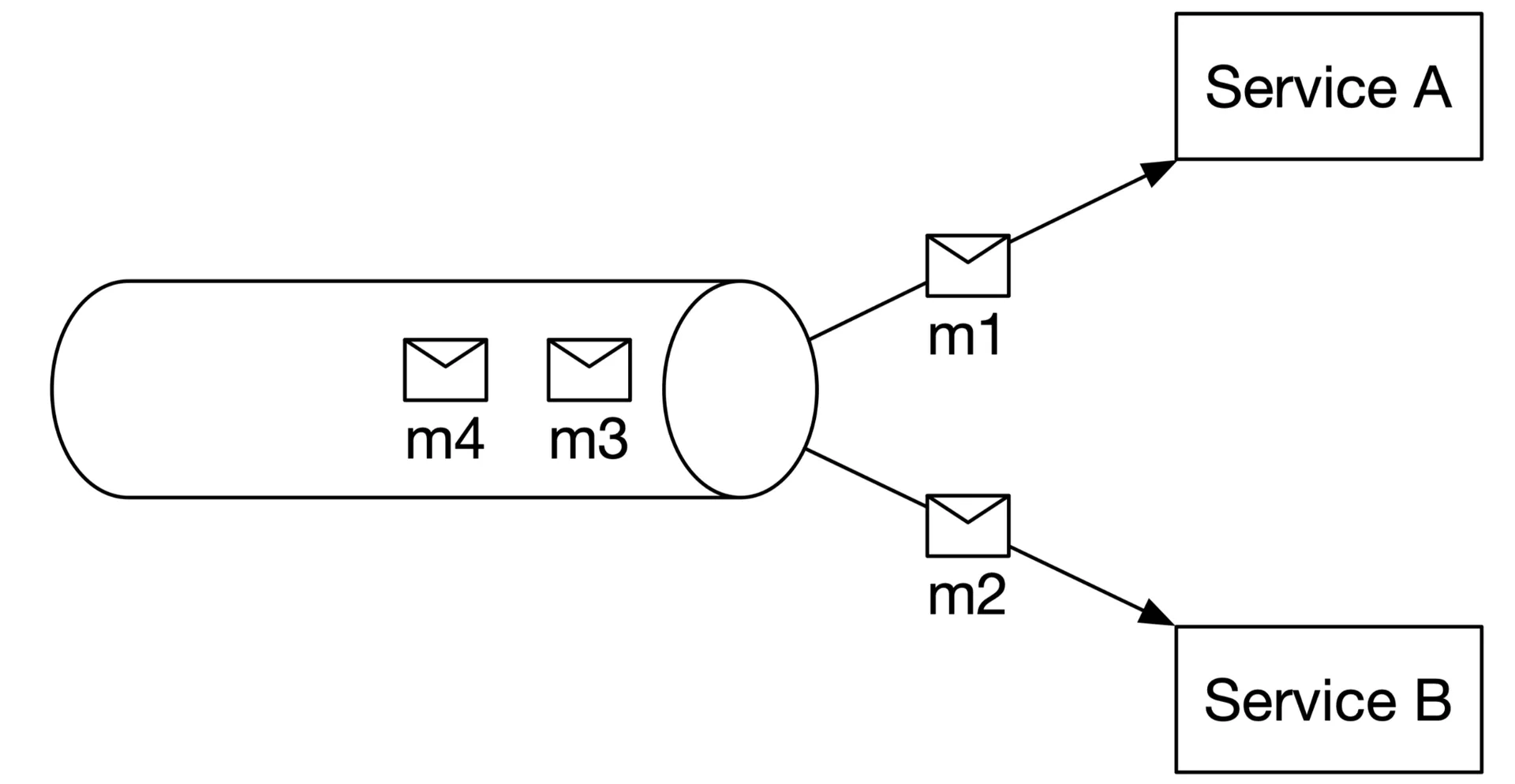

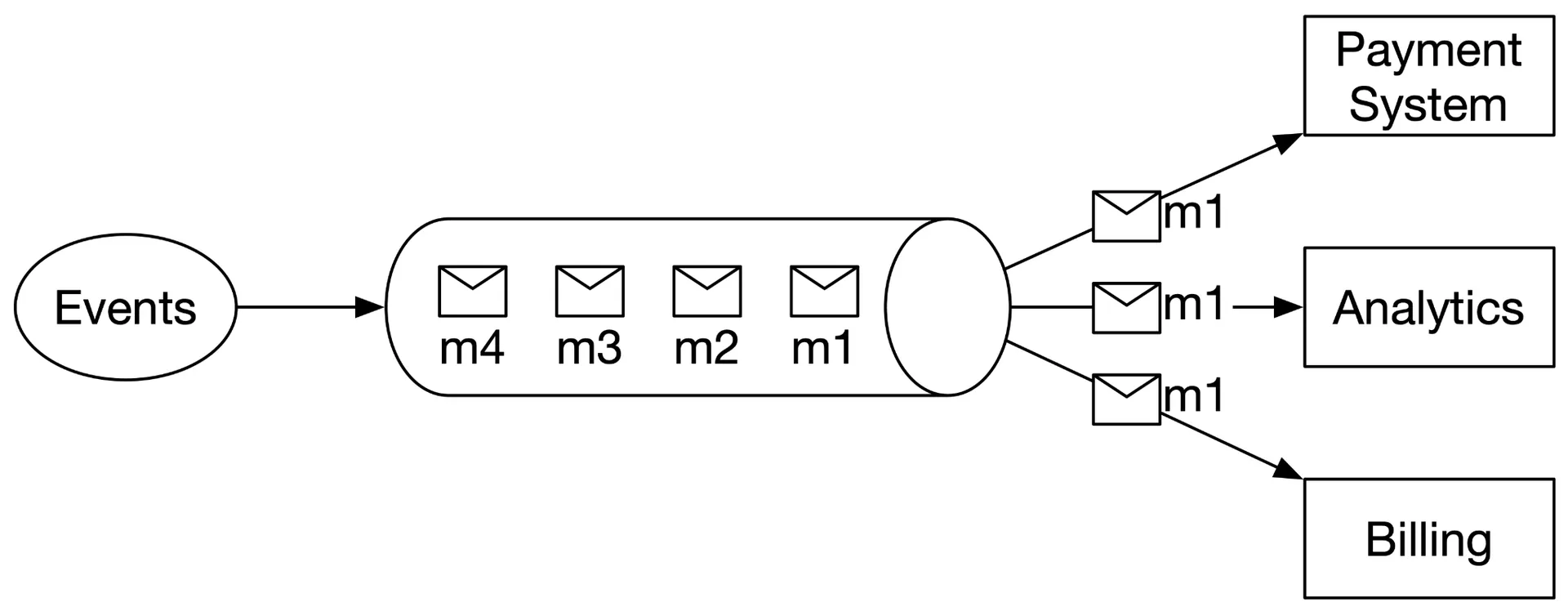

Multiple receivers: Kafka. Same message consumed by multiple services (payment, analytics, billing).

Figure 9: Multiple receivers

Figure 9: Multiple receivers

Sync = simpler but poor scalability. Async = trades simplicity for scalability + failure resilience. For large-scale payment systems with many dependencies → async preferred.

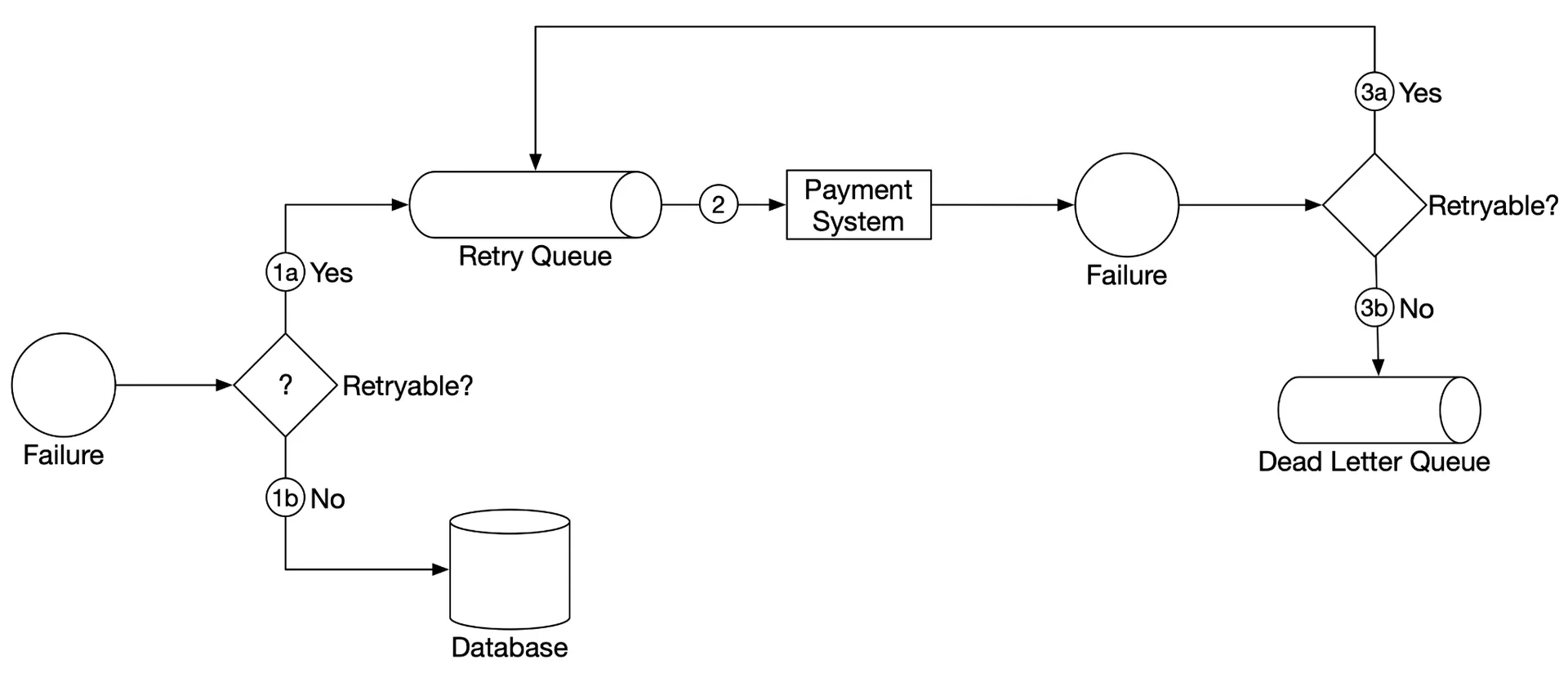

Handling failed payments

Track payment state: definitive state at any stage, persisted in append-only table.

Retry queue + dead letter queue:

Figure 10: Handle failed payments

- Check if failure is retryable

- Retryable → retry queue

- Non-retryable (invalid input) → error DB

- Consume retry queue, retry transactions

- If fails again:

- Retry count < threshold → back to retry queue

- Retry count ≥ threshold → dead letter queue (debug/inspect)

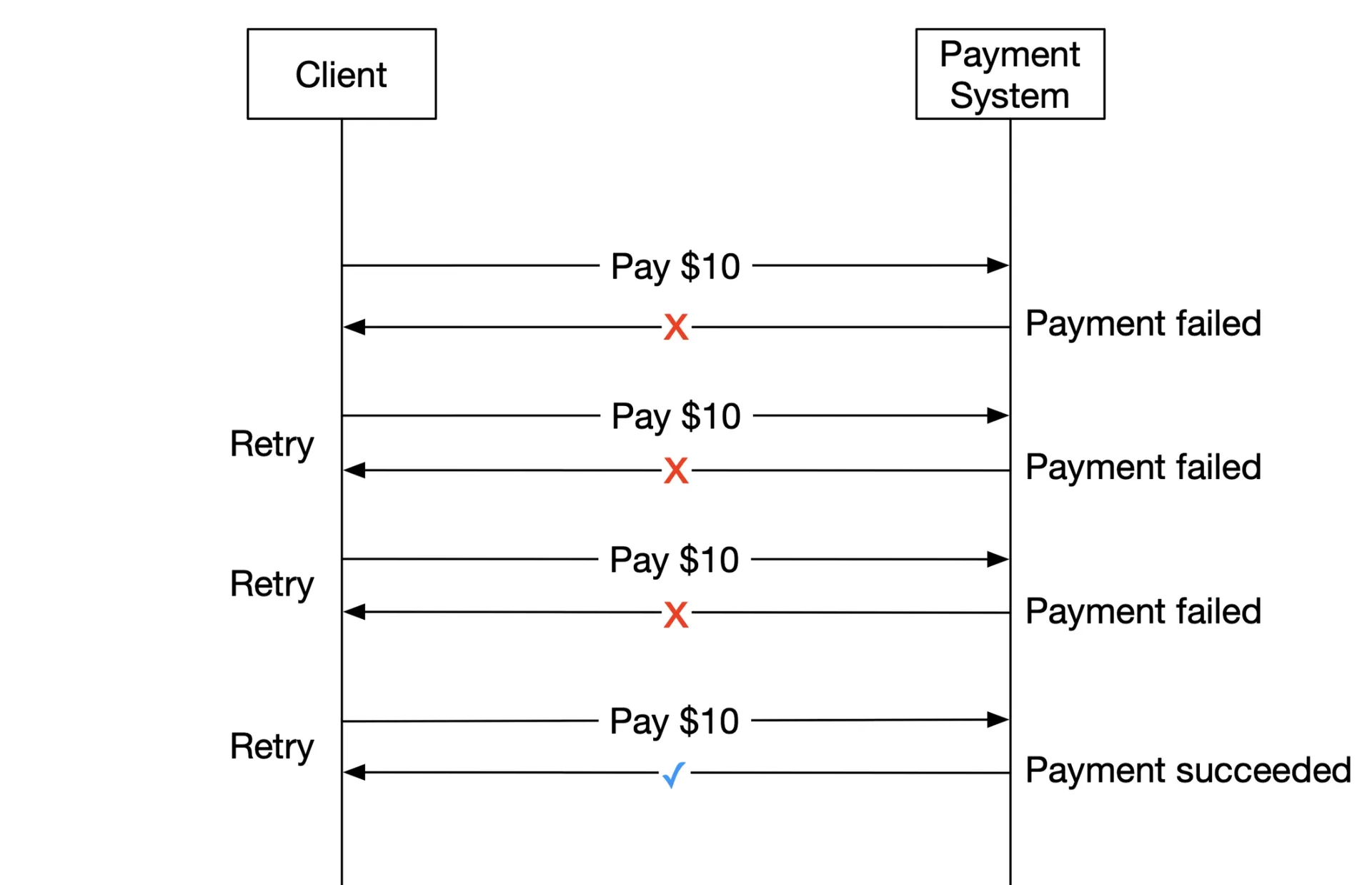

Exactly-once delivery

Exactly-once = at-least-once (retry) + at-most-once (idempotency).

Retry (at-least-once)

Figure 11: Retry

Retry strategies: Immediate, Fixed intervals, Incremental intervals, Exponential backoff (1s → 2s → 4s → ...), Cancel. Use exponential backoff for persistent network issues. Provide Retry-After header with error codes.

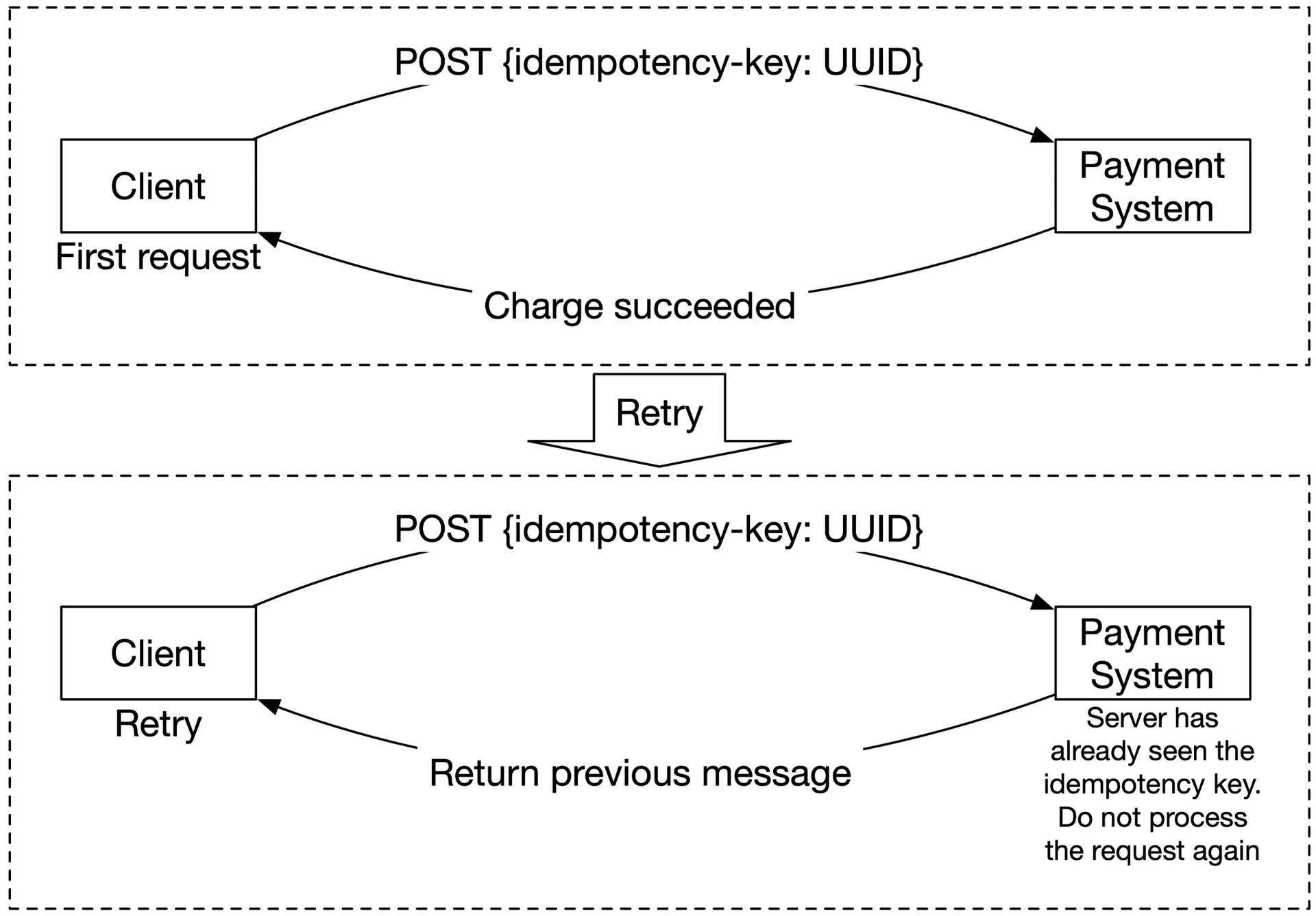

Idempotency (at-most-once)

Client generates UUID as idempotency key → HTTP header: <idempotency-key: key_value>. Stripe/PayPal recommended.

Scenario 1 (double click): idempotency key = shopping cart ID pre-checkout. Second request seen before → return previous request's status. Concurrent duplicates → 429 Too Many Requests.

Figure 12: Idempotency

Implementation: DB unique key constraint. Insert → success = new request. Insert fails (PK exists) = duplicate → reject.

Scenario 2 (PSP processed but response lost): nonce (payment_order_id) → PSP → token. Token uniquely maps to payment order. Re-send same token → PSP recognizes duplicate, returns previous execution status.

Consistency

Stateful services involved: payment service, ledger, wallet, PSP, DB replicas.

- Internal services: exactly-once processing

- Internal ↔ External (PSP): idempotency + reconciliation (never trust external system fully)

- Replica lag: Option 1: read+write from primary only (wastes replicas). Option 2: consensus algorithms (Paxos, Raft) or consensus-based DBs (YugabyteDB, CockroachDB).

Payment security

| Problem | Solution |

|---|---|

| Eavesdropping | HTTPS |

| Data tampering | Encryption + integrity monitoring |

| MITM attack | SSL + certificate pinning |

| Password storage | Salted hashing |

| Data loss | Multi-region DB replication + snapshots |

| DDoS | Rate limiting + firewall |

| Card theft | Tokenization (store tokens, not real numbers) |

| PCI compliance | PCI DSS standard |

| Fraud | Address verification, CVV, user behavior analysis |

Step 4 - Wrap Up

Designed payment system: pay-in/pay-out flows, PSP integration (hosted page), reconciliation (settlement files), async communication patterns, failure handling (retry + dead letter queues), exactly-once delivery (retry + idempotency), consistency, security. Additional considerations: monitoring, alerting, debugging tools, currency exchange, regional payment methods, cash payments (India/Brazil), Google/Apple Pay integration.